Saudi Arabia’s healthcare landscape is undergoing a structural transformation, with private hospitals increasingly emerging as the sector’s primary growth engine. The recently released 2024 data from the Ministry of Health, covering hospital activity across major cities, offers fresh insight into how capacity, demand, and competitive dynamics are evolving across the Kingdom, revealing that the gain in momentum is supported by demographic trends, economic development, and policy reform.

Private Sector Expansion Gains Momentum

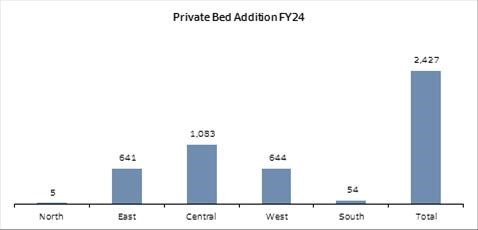

One of the most prominent themesin 2024 was the continued expansion of private healthcare providers, particularly in the Central and Western regions. These areas combine high population density, robust economic activity, and relatively strong purchasing power conditions that underpin sustained demand for higher-quality and specialized medical services.

The Central region remains intensely competitive, driven by ongoing population growth and the concentration of corporate and commercial activity. Meanwhile, the Western region continues to offer attractive opportunities, supported by religious tourism, large-scale infrastructure investments, and broader economic diversification under Vision 2030.

Private operators are responding decisively. Organic expansions, capacity additions, and targeted acquisitions are reinforcing their presence in high-demand urban centers, allowing them to capture both volume growth and more complex, higher-margin medical services.

Public Sector Growth and Budget Implications

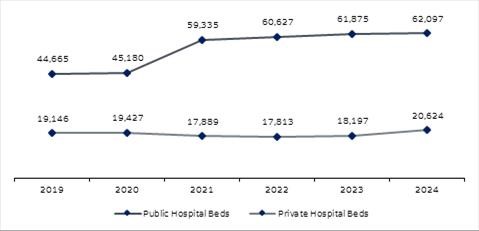

With public hospital capacity increasing in certain regions, it underscores the government’s commitment to improving access to healthcare, despite the growing fiscal burden associated with public provision.

Over time, the rising fiscal burden is likely to accelerate the enforcement and expansion of mandatory health insurance coverage. Greater insurance penetration would gradually shift healthcare funding away from direct public expenditure toward insured private care and would not only ease pressure on public finances but also support the long-term growth of private healthcare providers and insurance operators alike.

This evolution aligns closely with the Kingdom’s broader strategic objective of increasing private sector participation in healthcare delivery, improving efficiency while maintaining access and quality.

Lifestyle Shifts Favor Private Hospitals

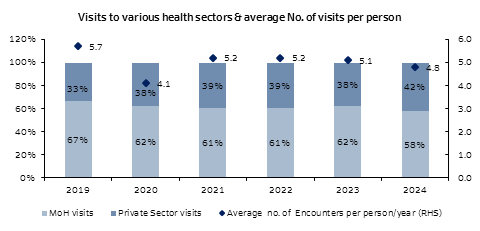

Beyond capacity and policy, patient behavior itself is changing. Rising income levels, greater health awareness, and increasing demand for faster and more specialized care are steadily shifting patient preferences toward private hospitals.

For private operators, this trend translates into higher occupancy rates, growing outpatient volumes, and stronger pricing power in select specialties. However, the same forces may pose challenges for insurance providers. Higher utilization and more frequent claims could pressure insurers’ loss ratios, particularly if medical cost inflation continues to outpace premium adjustments.

In essence, structural tailwinds for healthcare providers may simultaneously create margin headwinds for insurers, underscoring the need for careful pricing, underwriting discipline, and cost management across the healthcare value chain.

Rising Staff Costs: A Key Margin Risk

Despite the positive demand backdrop, profitability is not without challenges. Intensifying competition, especially in densely populated regions such as the Central region, is pushing up staff costs.

Competition for qualified medical professionals remains strong, and salary inflation is emerging as a key pressure point. As more hospitals enter crowded markets, wage escalation and retention incentives are likely to weigh on margins.

Operators with a) Strong brand positioning, b) Efficient cost structures, and c) Diversified geographic exposure are better positioned to navigate this environment.

Outlook

Overall, the 2024 data reinforces a constructive outlook for Saudi Arabia’s private healthcare sector. Structura ldemand drivers including demographic growth, lifestyle changes, and economic expansion remain firmly in place.

While rising staff costs and competitive intensity warrant close monitoring, the sector’s long-term fundamentals remain solid. Continued enforcement of health insurance and deeper private sector participation should further strengthen the industry’s trajectory.

As Saudi Arabia’s healthcare system continues its transition toward a more private-driven model, private hospitals are well-positioned to emerge as key beneficiaries of the Kingdom’s evolving healthcare landscape combining growth, resilience, and strategic relevance in the years ahead.