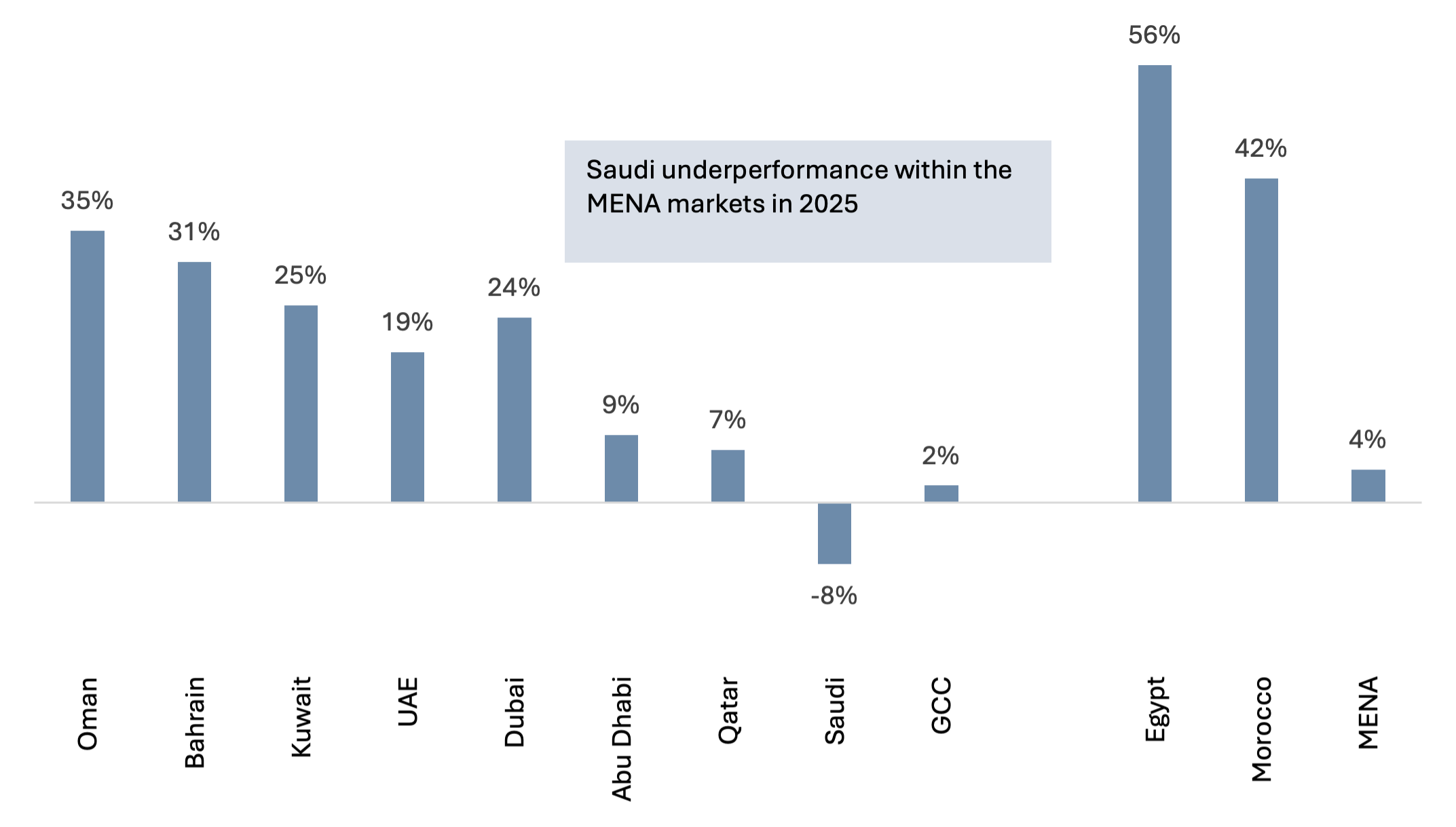

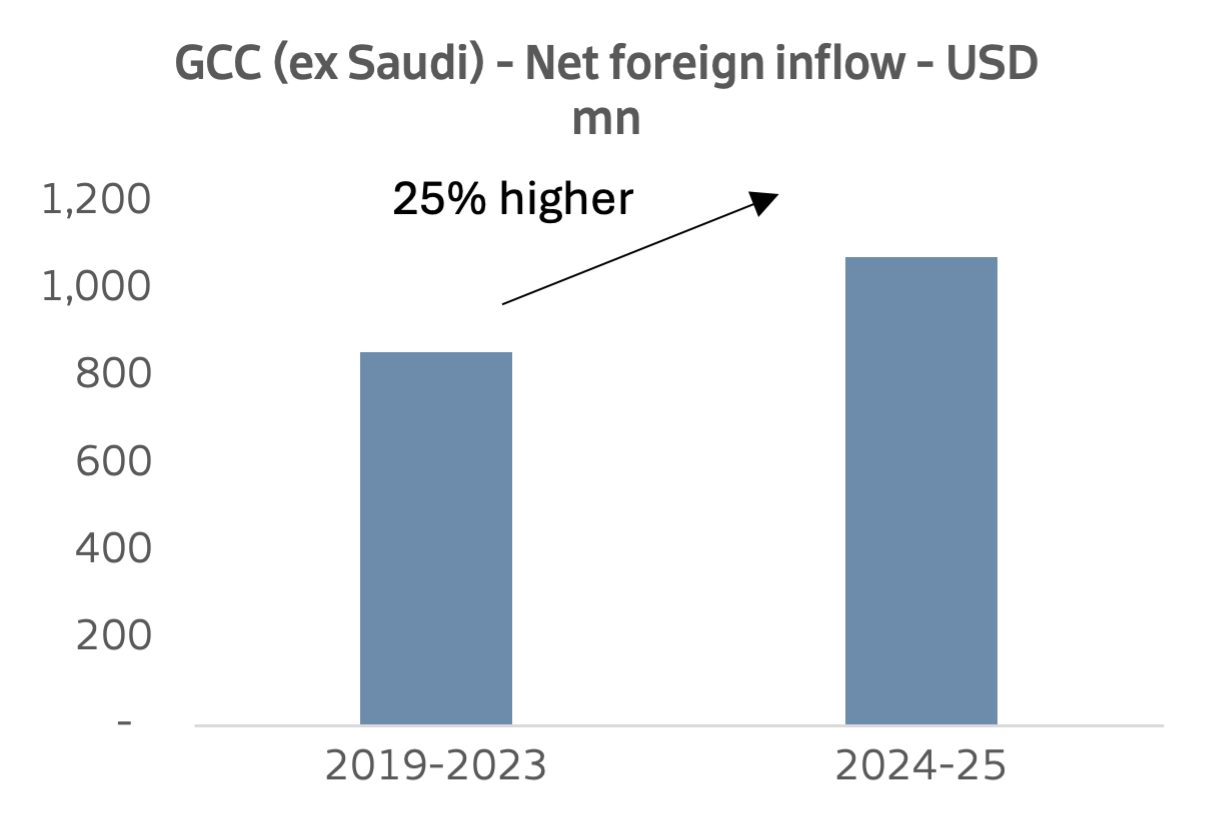

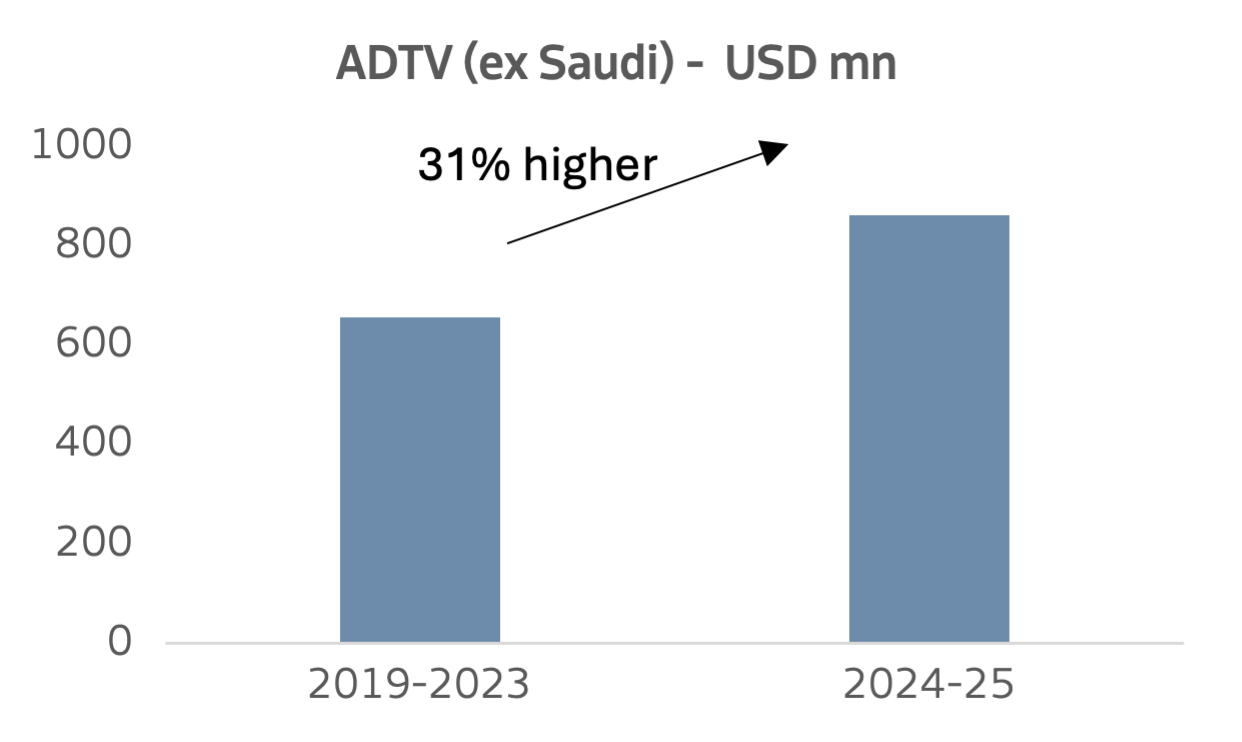

The past two years have clearly reinforced the importance and benefits of diversifying investments across the broader MENA region. The Saudi main market index, TASI, has underperformed other regional indices—particularly since the second half of 2024—driven by several factors. Among them are declining oil prices, rising fiscal deficit which led to a slowdown in government spending, and tightening liquidity, as a consequence of which corporate earnings growth moderated and pressured elevated valuations. In addition, global macro uncertainties weighed on commodity‑linked sectors such as petchems. In contrast, other GCC and wider MENA markets have delivered relatively resilient performance, each driven by market‑specific fundamentals such as structural reforms, economic momentum, earnings trajectories, and valuation dynamics.